Buying a home with no down payment and competitive interest rates is the hallmark of the USDA mortgage.

Buying a home with no down payment and competitive interest rates is the hallmark of the USDA mortgage.

What is the biggest obstacle preventing the majority of hard working Americans from buying a home? The answer is quite simple; a sufficient down payment. Most loan programs require at least 3.5% -5% and as high as 20% for a down payment. However, the United States Department of Agriculture (USDA) instituted a home loan program long ago to enable home buyers the chance to purchase a home without giving over a large chunk of their savings. Here are the general guidelines of the program.

First: Is the property located in an approved area?

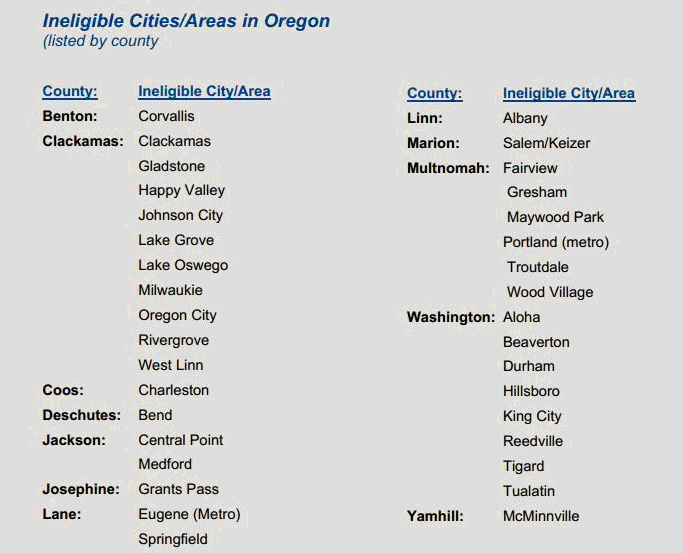

In order to qualify for the USDA funding a home must be within the limits of a particular area designated as rural. However, this is not a bad thing. There are numerous areas throughout Oregon that fall within the USDA rural areas. According to the USDA website, www.rurdev.usda.gov here is a list of the areas that are NOT allowed to use USDA financing for a home purchase:

Obviously the more populous areas, such as Portland and Beaverton, do not meet the criteria. But there are entire counties like Douglas and Polk where people can purchase a home using this wonderful mortgage program. If you have your eye on a home within a particular city and it is NOT in the above list then it should be eligible for the USDA mortgage. The un-shaded areas on this USDA loan eligibility map are eligible for the loan program. (When the page loads click “Single Family Homes” in the left column under “Property Eligibility”)

Second: Does your income meet the eligibility guidelines?

This mortgage is aimed at people with moderate to lower incomes. However, there are two rules about the income limit that are important to understand.

- The income limit is based on the number of people that will live within the home.

- The total income for all people cannot be higher than 115% of the median income base for your area.

Your mortgage broker can provide you with the income range for your area. Allowing people to use all of the people in the home to qualify can sometimes help since the allowable income is higher as the number in the household increases.

Along with meeting the income rules potential borrowers will also have to meet the debt to income ratio rules. Usually, the mortgage cannot be higher than 29% of the monthly household incomes before taxes are deducted and the total of all debts, including mortgage, cannot be more than 41%.

Third: Is the home the right type of property?

USDA mortgage loans can be used to buy an existing single family home. The borrower must intend to live in the home as their main residence. The home may be a new construction property. However, multiple family properties such as a duplex are not allowed. A condo may be approved if the building has been approved by the VA or FHA or if the structure is compliant with Freddie Mac or Fannie Mae rules. Mobile homes or manufactured homes are not allowed.

Fourth: What is the price of the home in relation to the appraised value?

We saved the best for last. If the sales price on the home is equal to or below the appraised value of the home, there is no requirement for a down payment. In fact, it is possible for the seller to pay 6% of the sales price towards closing costs and prepaid items. This will have to be negotiated with the seller and the real estate agents involved.

If you are one of the thousands of Oregon residents wishing they could take advantage of the historically low mortgage rates to buy a home, this is a wonderful way to become a home owner without the burden of paying a lot of money up front.